As consumers, each of us is fully cognizant of and deeply entwined with the “Information” economy.

Whether we use Google to search, shop on Amazon, connect with friends on Facebook or hail a cab using Uber, we hardly give a moment’s thought to the “building blocks” that have allowed these companies to achieve enormous success on a global scale.

Every organization today seeks to build enterprise value and drive growth through new distribution models, innovative products and services, enhanced customer experience and by harnessing advanced technologies. The fact that a few organizations stand out from the crowd, clearly indicates that their achievements aren’t easy to emulate.

In the banking sector, products, services, and customer interactions are geared towards both non-physical and (increasingly) real-time delivery. Hence, the opportunities presented by the information economy are truly enormous, and the risks of being marginalized are very real.

There is no doubt that banks have taken initiatives to capitalize on these opportunities, but my observations, both as a consumer and as a practitioner in the banking sector, suggest that these initiatives remain at a nascent stage. As the “possibility curve” shifts rapidly outward, banks that fail to take a holistic and pragmatic approach to rapidly building capability, will find themselves at a significant competitive disadvantage.

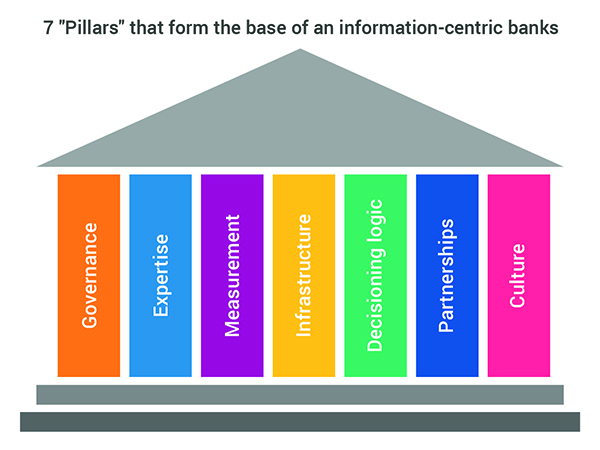

To make rapid progress that they desire to realise the value from the digital and data revolution, banks need to address the following 7 “Pillars” that form the base of any information-centric company:

1) Governance

While a bottoms-up, functional approach can deliver a quick start, to truly become an information-centric organization , it is absolutely essential to have senior leadership drive this endeavour with a cross-organizational mandate. They need to lock down strategic intent, assess status, prioritize initiatives and establish necessary processes across each pillar to achieve change quickly and at scale.

Navigating the rapidly changing landscape, maintaining a focus on customer centricity and ensuring that resource allocations are balanced across near and long term goals requires establishing and adhering to a highly disciplined management process .

2) Expertise

While the demand for “analysts” continues to increase exponentially, the term itself is used far too loosely. For large, global institutions, with hundreds of employees labelled “analysts” of some description, it is imperative to benchmark certain crucial skills, and to have appropriate recruitment and skill development processes in place.

In the absence of this, it is difficult for analysts spread across multiple functional disciplines (like risk, decision sciences, marketing, and operations) to harness their joint capabilities optimally.

3) Measurement

You manage what you measure.

Financial institutions have established detailed KPI’s (key performance indicators) for their businesses. However, if they are to accord with the need for speed, accuracy and relevance demanded by the modern consumer, they must be significantly refined and supplemented.

Additionally, Banks should look to a far deeper stratification of their existing MIS outputs to glean insights.

As just one example, while there is likely to be a wealth of data on customer selection , campaigns executed and overall results, it’s unlikely that there will be a formalized management information system (MIS) to ascertain the “cycle time” between a triggering event ( e.g. a purchase of a home) and the related marketing action.

Banks that execute marketing actions to reach a potential customer ahead of their competitors will clearly express distinction between the efficiency of their own activities and those of their competitors. More importantly, the customer experiences the two can boast of would be leagues apart.

4) Infrastructure

Upgrading the existing infrastructure to capture and harness the expanded internal and external data sets now available, is a necessity.

However, the notion that creating an ocean of information will in and of itself provide results is unrealistic.

Senior leaders must ensure that the infrastructure being built is aligned to specific strategic goals. That the level of investment and pacing is linked to the potential value that can be derived and, importantly, that this build out is aligned with progress on the other pillars

5) Decisioning logic

Advances in Artificial Intelligence are leading to the broadening use of machine learning to recalibrate responses in real time. Nonetheless, banks remain largely rooted in a static approach to building models that underpin their decisions across the customer lifecycle.

The existing processes to build models, validate their efficacy and deployment can take months, if not years. This cannot be the modus operandi going forward and will need to be revamped – without compromising on the requirements of a heavily regulated industry.

6) Partnerships

Considering the pillars noted above, it’s clear that financial institutions cannot address all of these, themselves.

Partnerships provide enormous value, on three major fronts – as sources of talent, expertise and relevant external data; as a supplement to internal resources and investment capacity,; and as a means to jointly create entirely new distribution systems , products and services

Sorting through the myriad of options being presented by third parties requires a disciplined approach, to ensure that FI’s are making optimal partner selection choices, while operating their business and optimizing value.

7) Culture

Although listed as the final item, it goes without saying that to become, and remain, a world class information-centric organization, it’s critical for FI’s to address the cultural changes that are desperately required.

Banks must shift their orientation from an ‘inward looking’ to an ‘outward seeking’ mindset. Management processes and incentives must be aligned to drive high performance, status quo approaches must be judiciously challenged, innovation must be fostered. Building and nurturing talent must be made imperative.

Summary

With few exceptions, banks across the world are struggling to meet their ROI and growth targets. Yet, there are myriad examples from other industries where organizations have challenged conventional thinking and generated enormous franchise value.

If banks can focus on driving change by embracing and executing against these seven pillars, they will position themselves for truly sustainable excellence.

P.S. Vikram Atal is writing a series of articles on banking-tech. This is the first article in the banking-tech series. So Stay Tuned!